Toast: Valuation

A few weeks ago, I covered CAVA. For no reason in particular, I’ve decided to stick with the restaurant theme and cover one of the “up and coming” service providers - Toast ( TOST 0.00%↑ ). Toast is hardly a new player in the space. They’ve been around since 2011, but have been winning market share and have started gaining real business momentum as of late...even while their stock price has floundered.

To explore more companies that I’ve covered, check out the full Corporate Valuation Catalog

Executive Summary

If all you do is read the Business Overview & Revenue Drivers overview, you’ll have a pretty good understanding of what Toast does and how they make money.

My overall findings are that Toast is probably about fairly valued today (at $30 per share) using modest, but optimistic growth assumptions. However, the investment comes with additional potential upside if management succeeds in their expansion efforts.

You should also check out the Risks section at the very bottom of the article because I highlight some interesting quirks about Toast’s business model and risks associated with the overall segment of the market they operate in.

Business Overview

Toast Inc. provides a cloud-based "operating system" built specifically to handle the unique, fast-paced demands of the restaurant industry. By unifying point-of-sale, back-office operations, and guest experience into a single platform, they eliminate the need for fragmented, disconnected tools.

Toast has historically targeted small to medium (SMB) restaurants, but has recently expanded their customer base to include larger enterprises like Applebee’s and TopGolf among others.

Today, Toast powers over 150,000 locations, and has been actively capturing market share.

Revenue Drivers

The first step is to understand how Toast makes money. Toast’s revenue is split into 3 categories:

I’ll cover these in more detail further down, but just to give a broad lay of the land:

Subscription Services start with the basic monthly rate that Toast charges for using their system - this fee is generally less than $100 per month (per location). In addition, there are add-on features like takeout, marketing & loyalty rewards programs, inventory management, hardware subscriptions (i.e., handhelds) and other “back of house” functions like payroll management applications.

Financial Technology Solutions (FTS) are split into two sub-categories. The first is payment processing. Every time someone makes a purchase and swipes their credit card, Toast collects a fee. A portion of this fee is divvied to the credit card company for transaction costs, while Toast keeps a slice for themselves. In addition, FTS also includes Toast Capital. Toast Capital is a program that lends money to restaurants. To-date, revenue generated by Toast Capital is a relatively small proportion of the total FTS pie.

Hardware & Professional Services (HPS) is primarily driven by the equipment and support needed to setup a new restaurant on the Toast network. This is generally considered a one-time transaction.

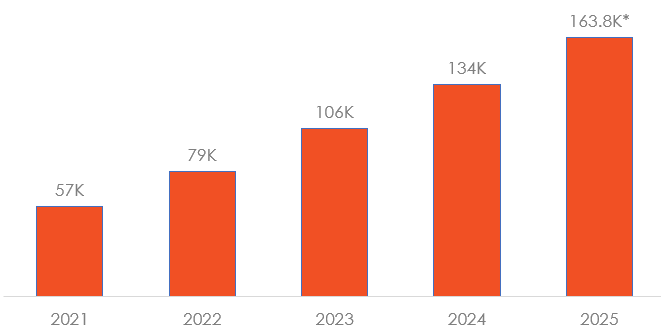

User Growth

Toast is expanding their user base. As of Q3 of 2025, they surpassed 150k locations.

Their primary focus has historically been small to medium sized restaurants. As of 2024, Toast has begun signing on larger & higher profile customers.

In addition, Toast has ambitions of expanding into other verticals: Food & Beverage Retail, Hospitality, and Grocery being the big ones.

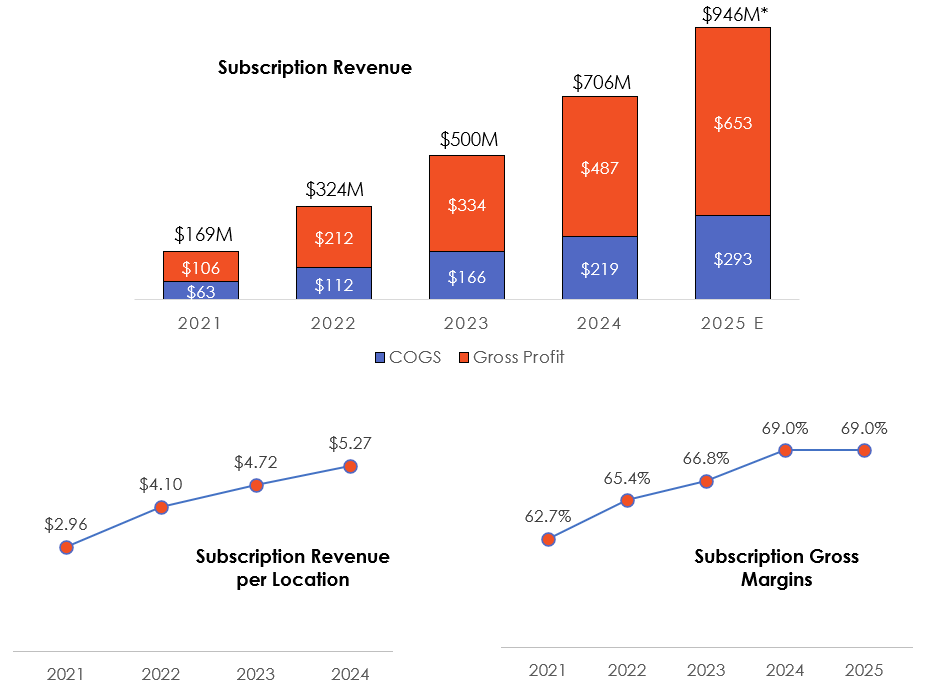

Subscription Services

Subscription revenue is derived from the base plan along with any add-on features that a restaurant owner might want:

This is the most straight forward category to break down. It’s recurring revenue that should scale relatively well with the number of locations.

Note that all 2025 numbers are estimates based on year over year growth as of the third quarter. Dollar amounts are all annual.

In general, we see subscription revenue climbing in compounding fashion - Toast is signing more customers, and customers are paying more on average (ARPU). ARPU (Average Revenue Per User) has been increasing due to price adjustments as well as upselling existing customers into more advanced features.