QS: Path to Commercialization

QS products have several avenues for reaching customers; I’ll try to cover the big ones here.

Joint Venture

This is the elephant in the room. QS and VW have had a JV in place since 2018. The JV, dubbed “QSV”, is already established with capital contributed by both sides - albeit a very tiny amount of capital. The details are pretty vague at the moment. Much of the JVA documentation highlighting the terms of the agreement are redacted. But QS management has given us plenty of hints in regards to the eventual structure of the deal.

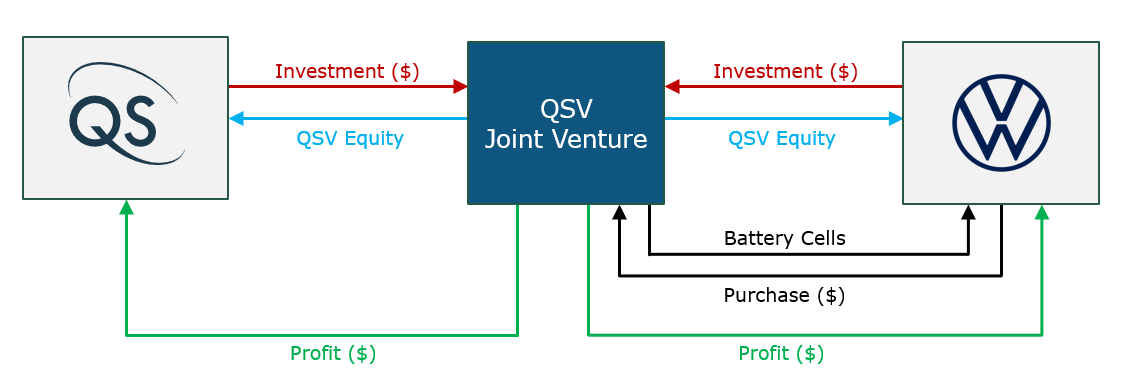

Figure 1 illustrates the baseline arrangement. Basically, both QS and VW will fund (red) a stand alone company called QSV. In turn, they’ll each own a 50% stake in the company (blue). That company will sell cells to VW (black) at market rate. Any profits that QSV makes will flow back to the parent companies (green) in proportion to their ownership stakes.

Where it gets interesting is figuring out where QS will come up with their portion of the investment funding. Giga Factories can cost billions of dollars, and by the time QSV is breaking ground, Quantumscape will have chewed up much of the remaining cash currently living on the balance sheet - management estimates early 2026 is the current cash runway.

The obvious avenues are equity dilution or debt. I actually think debt financing might be difficult to obtain because of the nature of the business structure. QS would probably need to obtain capital without using their stake in QSV as collateral. VW may not go for leveraging up the opposite half of their business.

This venture could actually become quite incestuous with VW taking another ownership stake in Quantumscape, basically funding QS’s side of the venture. This could be in the form of debt financing, but will likely be structured similar to Rivian’s recent deal with Volkswagen. VW already owns nearly 30% of Quantumscape. Something like this opens the door for VW simply acquiring QS, which isn’t ideal for QS shareholders.

Alternatively, VW could simply own a bigger portion of the Joint Venture, and with it, a bigger slice of the profit pie. The split could be something like 70/30 instead of 50/50. Quantumscape’s cash outlay will be reduced, and they still get the benefit of gaining know-how in setting up a large scale facility.

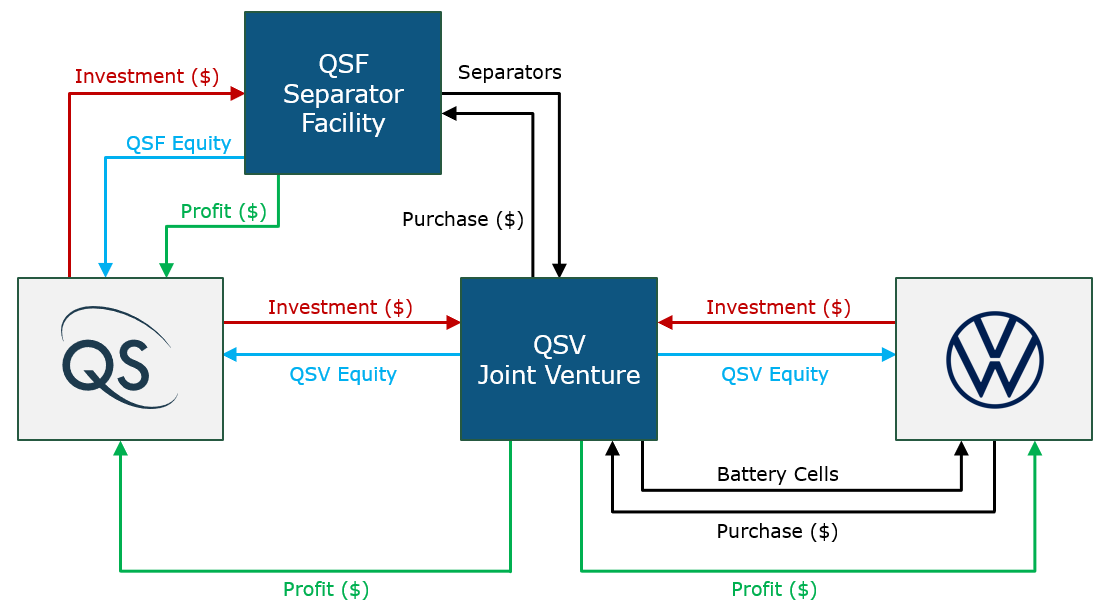

Quantumscape management has also discussed the possibility of keeping the JV in its current form, but breaking out the separator production line. Basically, becoming a separator supplier to the JV currently in place. See Figure 2. Note that this is drawn as if the separator production facility (QSF) is its own entity, with QS having a 100% ownership stake in QSF. Even if this is not the case, it effectively works like this, and is easier to visualize and analyze. In fact, as I move forward with valuing QS, I’ll probably conceptualize each giga factory as a standalone company even if its not structured that way in the filings. It will make analysis easier by allowing for “sum of the parts” methodology.

There’s actually a couple of advantages and disadvantages to this:

Advantage. Quantumscape could more easily finance QSF through borrowing. They would likely be able to use the equipment and facility as collateral without needing VW’s approval. This structure gives QS a lot more flexibility in funding that portion of the operation.

Disadvantage. Quantumscape’s total investment will actually be higher in this arrangement. In the “straight-line” JV, VW would effectively fund half of the separator facility. Breaking QSF out will require Quantumscape to eat that entire portion of the manufacturing line.

Advantage. Depending on how the deal is structured, QSF could probably expand beyond the needs of QSV (and VW), allowing them to sell separators to other OEMs.

Disadvantage. This could make some of the accounting hard to track. For instance, if the separator manufacturing is set up as a “factory inside a factory” as management has alluded to in the past, then QSF would likely need to lease their space from QSV.

Note, I’ve created the moniker “QSF” as a short hand for QS Film (or Separator) Facility. This hasn’t been discussed by Quantumscape, and you won’t find “QSF” anywhere in any official filings or management commentary.

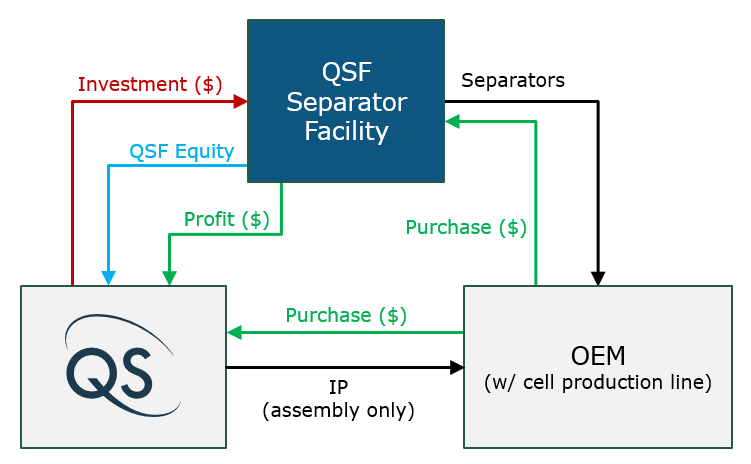

Separator Supplier

This is another commercialization avenue that management has discussed. It would be much less capital intensive than building out entire cell production factories while still protecting the “secret sauce” that is the separator recipe. See Figure 3.

This comes with a lot of the advantages discussed above. QS would deliver finished rolls of films and license the flex-frame format and assembly process. As discussed, briefly, in the Unit Economics post, QS should still capture much of the profit that would come had they manufactured the entire cell. The value is in the technology.

Cell Manufacturer

This is the most streamlined setup. QS would manufacture and deliver the entire cell. This is the most capital intensive path to commercialization, but it puts QS in the driver’s seat for future development and expansion.

Manufacturing and delivering completed cells would also be the most profitable on an absolute basis.

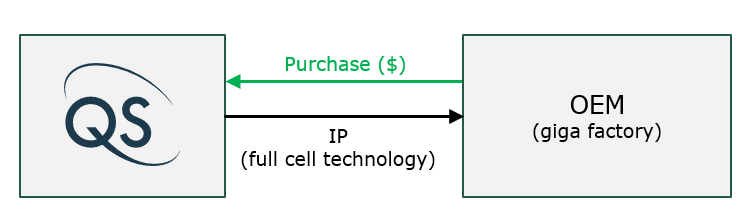

Licensing

Licensing the full IP package would be the cheapest and safest path to market for QS.

They would assume none of the risk in regards to setting up and scaling a factory, but should still capture much of the profit they would have otherwise. Again, the value is in the technology.

I would be curious how this commercialization structure would work…

One way is that it could be set up on a royalty structure where QS gets a cut of each delivered kWh of production. From my Unit Economics post, we estimate that QS’s potential profit could baseline at around $27 per kWh if they were to deliver fully completed cells. Under a royalty agreement, maybe QS receives $10 to $15 per manufactured kWh from the OEM.

Another way is simply a flat annual rate. One advantage to this deal structure is that QS bares no risk in the event that an OEM bungles up their operations. The obvious disadvantage is that QS wouldn’t capture any of the scale. OEMs could add capacity with no additional gain going to Quantumscape.

I haven’t researched how this type of deal structure works in this industry (or others) yet, so I don’t have a good corollary to work off of. That might be worth digging through more as I progress through my valuation exercises.

IP protection becomes a growing concern with this deal structure.

Summary

These are just a few ideas on how management has portrayed their different paths to commercialization. I think my next step is to really dig into the costs of constructing a giga factory, and the ways other companies have financed that endeavor. The biggest risk-elephant in the room is how they’ll actually fund themselves beyond 2025. Without a major advance in the stock price, QS may be pretty limited in their options.