Joby: Valuation

Sanity Check

I’m planning on performing a detailed valuation at a later date, but I wanted to take a shallow look at it, now, after the stock’s recent surge of 230% off the April lows to see what exactly is being priced in at the moment, and whether we should be buying more here or looking to trim.

Unit Economics

I’m only really going to consider their at-scale unit economics. I’ll focus primarily on their Ohio production rate (500 aircraft per year), and ignore the Marina Facility (24 aircraft per year).

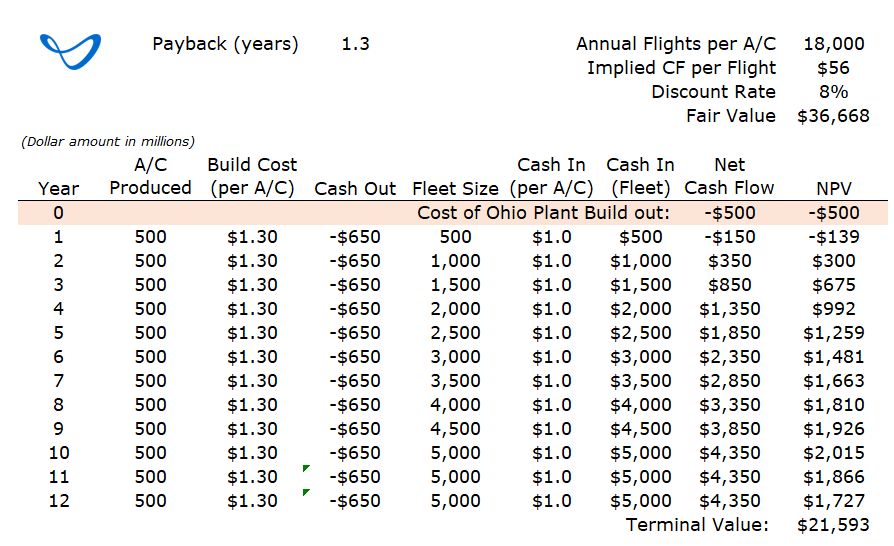

Joby estimates that their aircraft will cost about $1.3 million and produce about $1 million in net profits per year (with a payback period of 1.3 years).

On a per plane basis, at a price point of $3.00 per seat mile by 2026, we anticipate each aircraft will generate approximately $2.2 million of net revenue, which when combined with the all-in favorable unit cost profile, will generate approximately $1.0 million of earnings. This creates an attractive payback period of just 1.3 years for an aircraft with a projected 10-year service life, and demonstrates the compelling opportunity we have to increase scale.

2021, S-1 Filing

Fleet Size

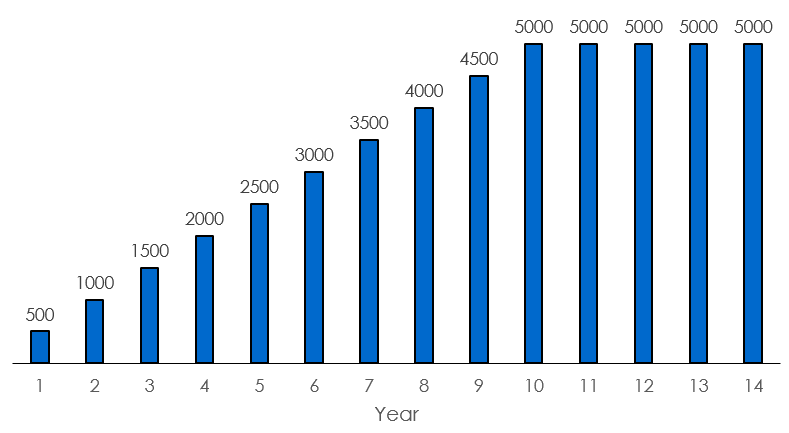

It’s also important to note the service life because we’ll need to factor in attrition of their aircraft. For example, once they spool up their Ohio production facility, producing 500 aircraft per year, their fleet will grow by 500 aircraft every year (500, 1000, 1500, and so on).

However, by year 10, the first batch of aircraft will reach end-of-life, and every new unit going into service will go towards replacement of a retiring aircraft. The implication is that the fleet size (that’s supported by the Ohio plant) will top out at around 5,000 aircraft.

Valuation - Direct to Consumer

Using the unit economics from above ($1.3 million aircraft cost & $1 million in annual cash flow per aircraft), we can build out projected cash flow.

Note, this only considers the economics of the Ohio plant & Joby air taxi service, and excludes any R&D and SG&A activities at the corporate level.

The resulting valuation is a market cap of $37 billion (which is still more than double the current market cap - $15 billion at the end of July, 2025).

There are a couple of interesting insights we can glean from this calc. First, Joby’s net cash flow per flight would be about 56 dollars assuming that they’re flying 3 flights per hour, 18 hours a day (or about 18,000 flights per year). This leaves operational cash flow margins in the 15% to 20% range.

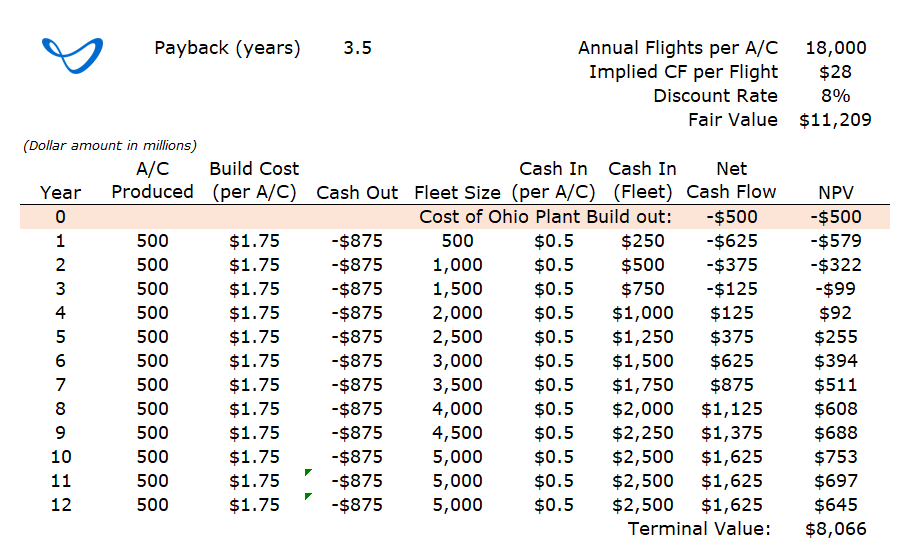

This is obviously highly sensitive to the build costs, payback period, and service life. If we were to ‘abandon’ their projections (from 2021, btw) and assume that build costs will be $1.75 million (instead of $1.3 million) and annual cash flow from aircraft operations is $500k (instead of $1 million), we get this:

While more muted, this still offers a valuation above $11 billion. Operational cash flow margins would be in the 8% to 10% range here.

More work needs to be done on the unit economics estimations to truly get a handle on Joby’s potential cash flows. And I would imagine projecting out things like autonomy would really change this math.

All-in-all, I would say that today’s market pricing has pretty effectively priced in the Ohio plant production coming online…especially once we consider that this plant won’t truly spool up for another few years and there’s still a lot of R&D activity and TC support work going on right now (all of which we haven’t discounted for, here).

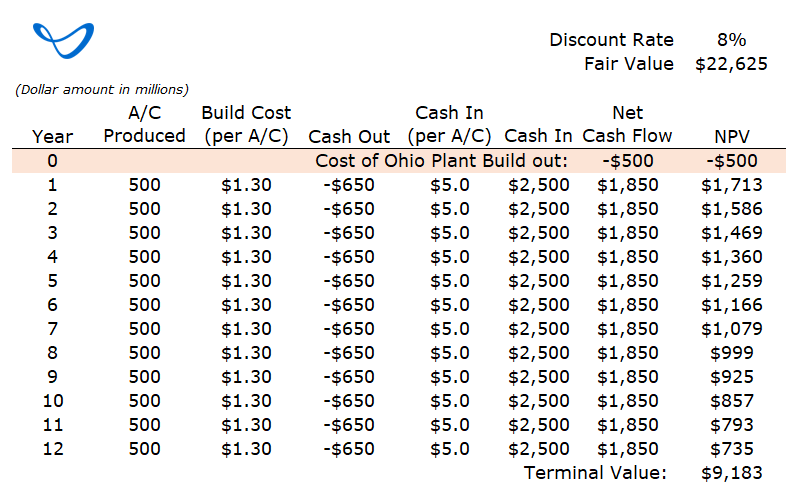

Valuation - Aircraft Sales

Joby has disclosed that they will pursue a mixture of operating their own fleet and aircraft sales directly to customers. One potential customer is Toyota who has ambitions of starting their own air taxi service.

I don’t know if there are any official numbers for sales price out there, but I know that other companies have been targeting $5 million per aircraft.

Figure 4 runs the numbers with only direct aircraft sales.

Other Considerations

Here are some other things to chew on in the meantime.

Service Life

The implied service life is close to 200,000 flights (10 years at close to 20,000 flights per year).

There’s not another aircraft, that I know of, that has a service life in this realm. Boeing aircraft are considered workhorses in the aviation world, and they’re only good for between 50k & 70k flights.

We’ll see what kind of maintenance schedules these aircraft have, but color me a little skeptical; I would say 200k flights is ambitious, at best, and straight up whimsical, at worst…especially for a brand new aircraft type where there aren’t really any operational data to pull lessons-learned from.

Growth

This valuation is for the single production facility in Ohio that will supposedly produce 500 aircraft per year and support a global fleet of about 5,000 units.

JoeBen has previously stated that he sees the addressable market in the millions of aircraft. Even if you think that’s way too optimistic, there’s a lot of room to split the difference between 5,000 units and millions. It’s likely that Joby will expand production incrementally over time.

Running the numbers, and assuming that Joby adds 500 incremental production rate every 5 years or so, it doesn’t take much to get to a $40 billion valuation (or higher). Obviously it’ll depend on the fleet size that the market can handle.

In addition, we don’t factor in inflation or any other potential bottom-line growth drivers. Autonomy would bring operational costs way down. Energy costs may come down in the future. Improved battery performance and energy density (or hybrid powerplants) could increase unit up-time and range - less time charging, more time flying.

Right Tails

Just to expand on the subject of growth, Joby has a lot of other ideas in the works:

They’re supposedly working on hydrogen aircraft, both an S4 hybrid variant and perhaps fixed wing (?)

Autonomous aircraft could slice operational costs in a major way

Broader market adoption and increased TAM

If a company is fairly priced, but doesn’t consider right-tails, then it’s not fairly valued at all - it’s undervalued.

Risks

We also really should consider the black swans that could hit this company.

One or two serious incidents could spoil this market for a very long time. Once they let these out into the wild, that’s always a risk… This even applies to the scenario where a competitor has a mishap.

Joby still hasn’t achieved Type Certification. While this risk diminishes with every completed milestone, we shouldn’t consider it a given.

Adoption could be muted due to poor air traffic management.

If service life is much shorter than 10 years and 200,000 flight cycles, the business economics would change immensely. Fleet size would be smaller. “Per Aircraft” value would fall, precipitously.

One way to factor in risks is to increase the discount rate. I’ve used 8% for all the valuation calculations in this post (which I consider to be the market rate). This is probably unconservative.

If you wanted to use a CAPM method, you’d get a cost of equity of about 14%. Plugging that into Figure 2 (upside scenario), we’d get a fair value of about $16 billion which is pretty close to today’s market cap of $15 billion.