I’ve begun writing my first pass at actually attempting to come up with an intrinsic value for Quantumscape. In doing so, I’ve discovered that there are a few important concepts that the reader should be familiar with heading into that report. Rather than bogging that post down with filler explanatory dialog, I thought it would be useful to do a quick explainer here, and just refer back to this post.

This concept is important because we need to be able to value the combination set of different potential outcomes. See Figure 1 for a sample of Quantumscape’s probability tree.

Each scenario has a designated likelihood of happening at any moment in time. We can use each scenarios probabilities and expected values to value the company.

I’ll illustrate this concept below using coin tosses and dice throws.

Betting on a Coin Toss

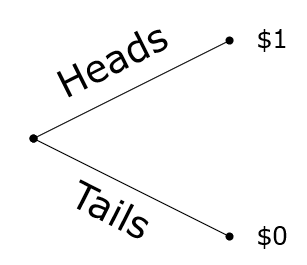

Imagine wagering on a coin toss that pays out $1 if you win, and nothing if you lose. How much would you be willing to bet?

We know from intuition (or experience) that the bettor in this scenario has a 50/50 chance of winning, so we would want to at least double our money if we win. That makes the fair value of this particular game $0.50.

In probability theory, this is known as the “expected value”. Or the value you expect to win, on average. Of course, you’ll never actually win fifty cents (since the pay out is either one dollar or zero), but you will expect your total winnings per play to average fifty cents.

And of course we can visualize this by drawing the probability tree:

The expected value calculation is shown as:

P(H) and P(T) are the probabilities for flipping heads and tails, respectively. Knowing that probability of flipping heads or tails are each 50% (or 0.5), we can solve for the expected value.

If this were investing (which, in a sense, it is), the fair value of this coin toss is $0.50 (confirming our intuition from above).

Bringing this back to Quantumscape for a second, we know that the outcomes aren’t completely binary in this nature. There are outcomes where a “loss” doesn’t have a zero pay off (there’s residual value of the IP, for instance).

Making this analogous to our coin toss, we could imagine the payoff for flipping heads as $1, while the payoff for flipping tails is $0.20.

In this scenario the expected value would be:

The takeaway here is that now a bettor should be willing to wager up to $0.60 to play this game before losing their edge. Fair value is $0.60 in this context.

Betting on a Dice Throw

Betting on a dice throw works in the exact same way, but now with differing probabilities.

Say there’s another game where rolling a three with a single dice pays off a dollar.

The expected value is calculated the same way as we did for the coin toss.

The odds of flipping any particular number is 1/6

So the fair value to play this particular game is just over sixteen cents. We could do the same exercise as the coin toss where we assign different values to different outcomes, but we’ll skip that for now.

Combining Events

Now imagine we have a parlay where we flip a coin and then roll a dice. If we flip heads and roll a three we win a dollar, otherwise we win nothing.

First let’s calculate the odds of actually accomplishing this endeavor.

For two independent events - i.e., the coin flip outcome has no bearing on the probabilities of the dice throw - the probability of the two events occurring is simply the product of each probability.

Given that we know the probabilities of both of these events are 1/2 and 1/6, respectively, we know that the odds of both events occurring in one game is 1/12 (or 8.33%).

And the expected value:

So we see that if we require these two events to happen, the “fair value” of the game is greatly decreased.

Again, we could assign differing values for each outcome, but the general procedure is the same.

Summary

This is meant to be a quick introduction, and not an exhaustive manual on probability. You can find a much better course on probability theory online. I just wanted to familiarize the reader with this concept because I’ll refer back to it frequently in my valuation.

Tying this to valuation, this is especially important for startups or pre-revenue companies. A company like Quantumscape, for instance, will either succeed in reaching commercialization or they won’t. The competition will also succeed or they won’t. These two events are largely independent of one another. And the array of outcomes each have their own assigned probabilities and values.

For instance, Quantumscape’s probability tree might look as follows (copied from Figure 1):

The trick will be estimating the probabilities and valuations for each particular outcome. Then we can ‘solve’ for the company’s intrinsic value following the same method as described herein. This will all be demonstrated in my next valuation post.

Added Bonus: any event that changes these probabilities (such as the PowerCo agreement) will result in a discrete change to the valuation (seen as a jump in the stock price). See Anatomy of a Catalyst for more color.