Amprius

I’ve previously presented a lot of analysis for Quantumscape, but I haven’t really shown how they stack up to other next-gen technologies….which is a very important consideration. After all, a big component of the valuation for these companies is tied to the probability that there are only one or two winners in the space.

Today, I’ll be covering Amprius ( AMPX 0.00%↑ ) which is a company that I consider to be a front runner in the next-gen battery space.

I currently own no shares of Amprius and own a decently sized position in a potential competitor, Quantumscape - this provides helpful context regarding my potential biases.

To explore more companies that I’ve covered, check out the full Corporate Valuation Catalog

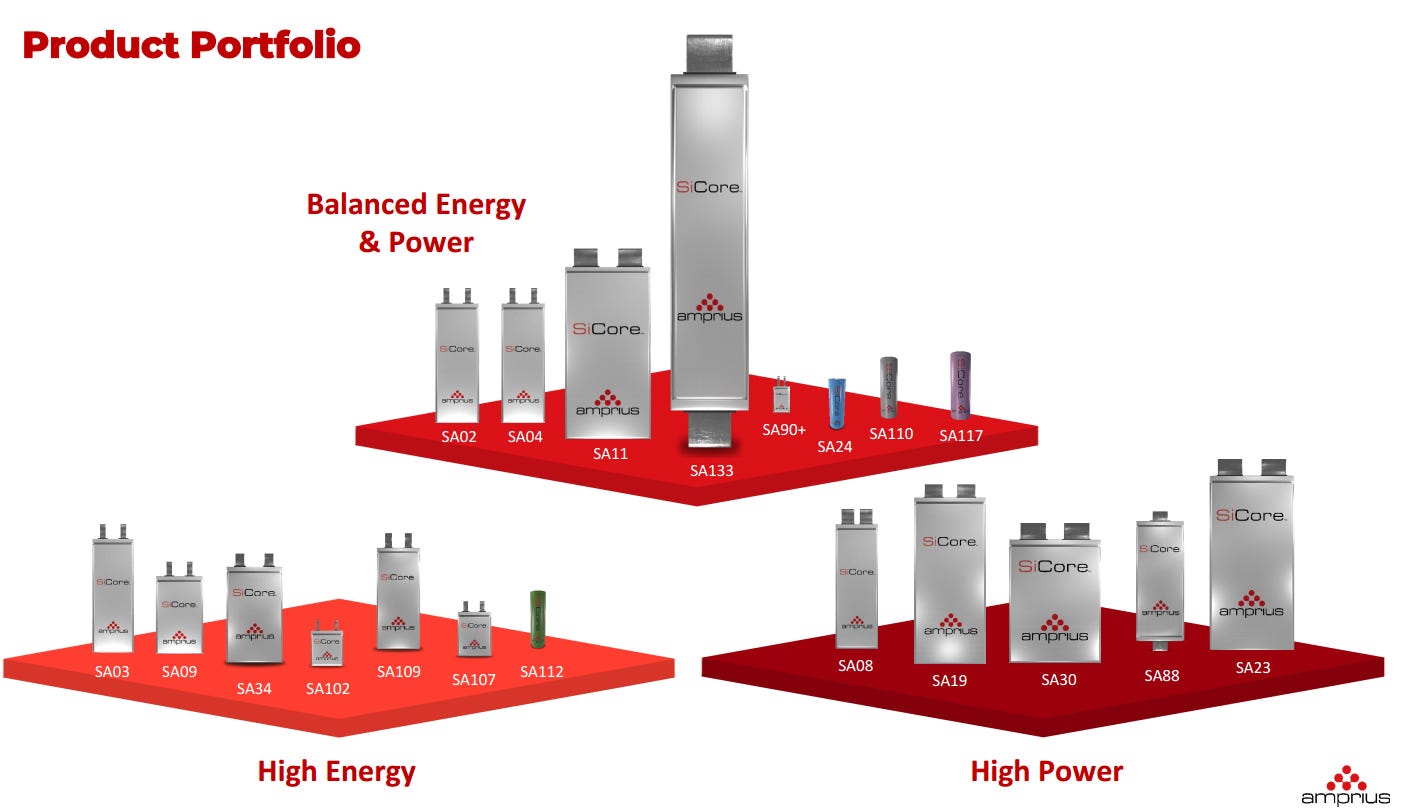

Product Overview

Unlike other players in the industry, who offer a lot of hope and promise, Amprius has real products that they’re selling to real customers…right now.

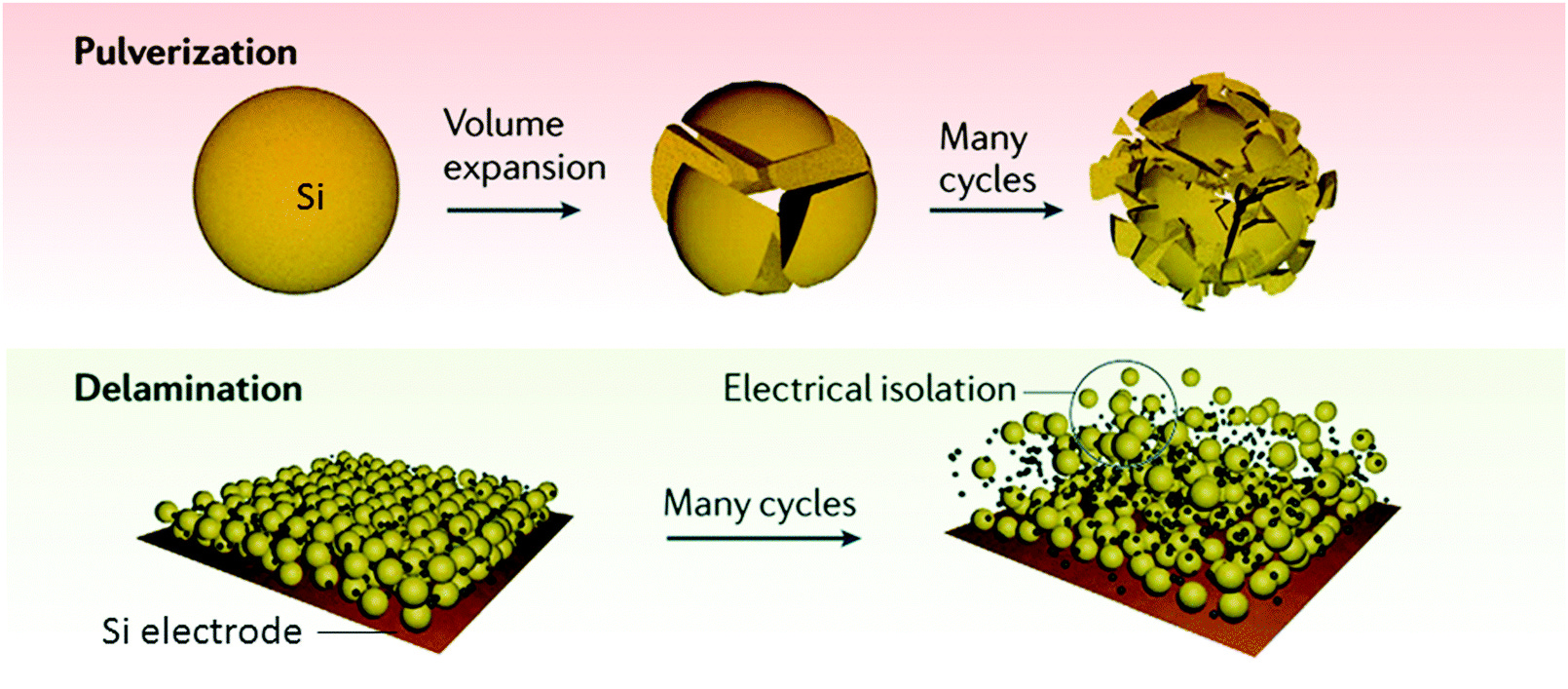

Their core product is based around silicon anodes. Like lithium metal (which Quantumscape is pursuing), silicon offers a similar step change in cell level energy densities. The big problem with silicon, however, is that silicon can expand nearly 300% during charging, which presents an interesting engineering challenge where the silicon can basically destroy itself - this is known as pulverization:

Amprius came up with a quite novel solution for this. Their first product, SiMaxx, uses silicon nanowires in the anode, spaced in such a way as to allow expansion and avoiding the pulverization problem.

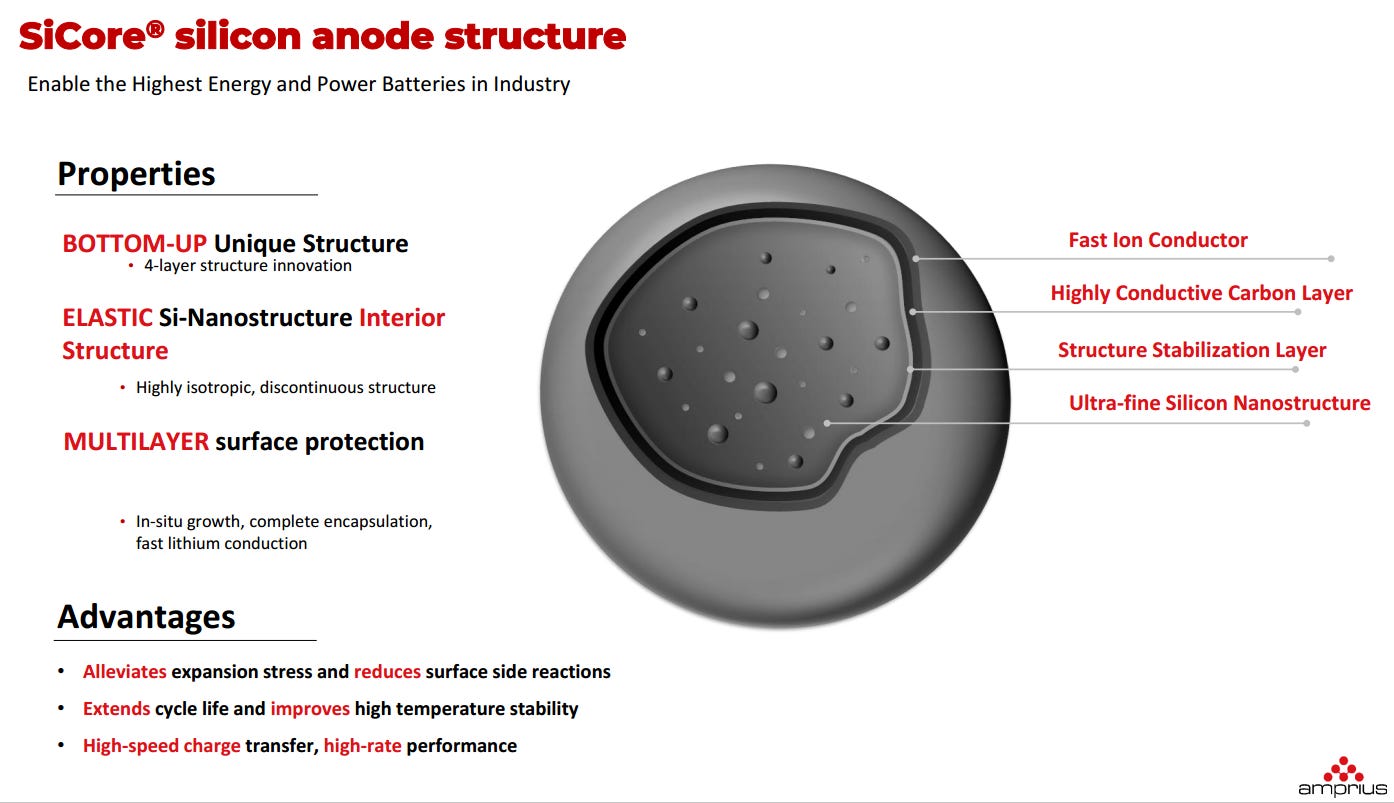

They’ve since iterated towards their second generation product, SiCore, which follows the same theme of designing around silicon expansion, but I believe ditches the nanowire design:

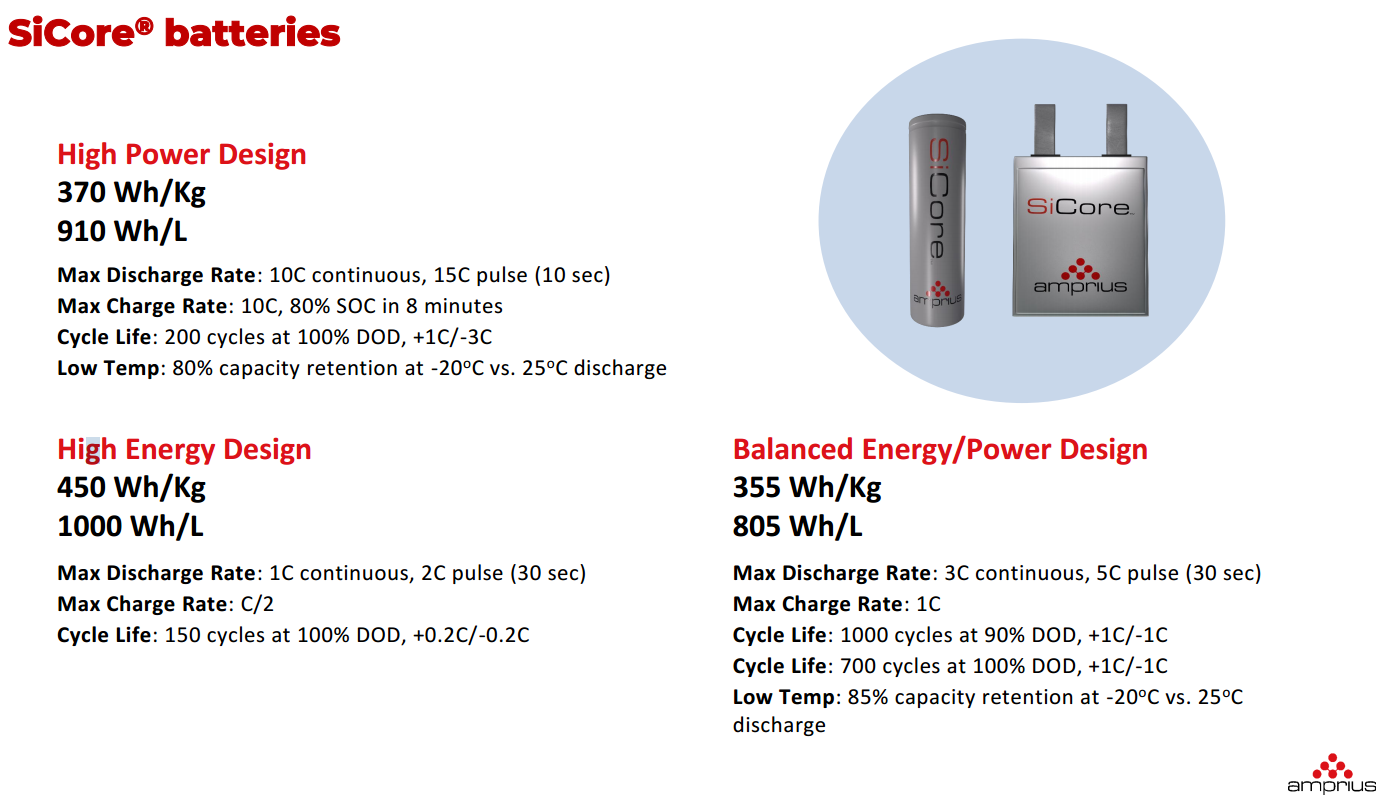

Product Specs

Amprius regularly touts their “up-to” specs. In press releases, you’ll often see something to the effect of “Amprius batteries offer energy densities up-to 500 wh/kg, charge rates up-to 10C, and cycle lives up-to 1200 cycles”.

However, no product offers these combined specs. This is a trap I frequently see investors fall into, thinking Amprius has cornered the perfect battery when really, these cells come with a lot of trade-offs.

Figure 5 shows that their high energy density cells sacrifice cycle life (150 cycles with 5 hour charge times) and charge times (max rate of 2 hour charge). Likewise, their power cell only last 200 cycles.

Product Market Fit

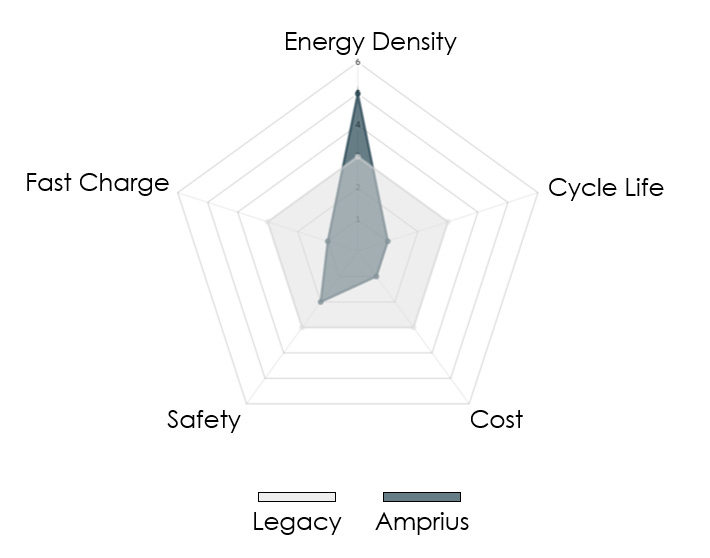

The first thing we should look at is how these cells stack up against existing solutions on the market. If we think about this more qualitatively, we can compare against traditional / legacy graphite anode cells (see Figure 6).

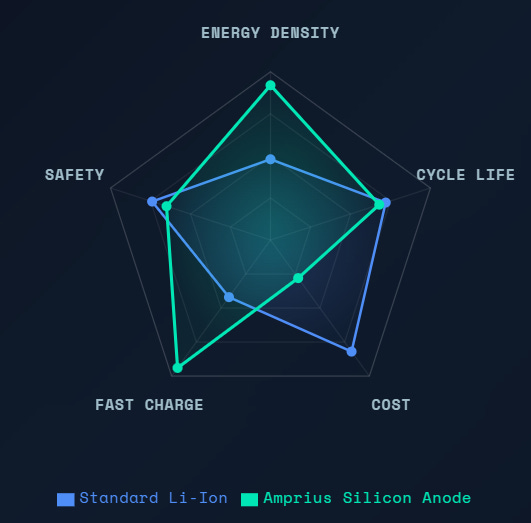

Figure 6 shows Amprius’ energy solution vs the typical li-ion EV cell (NMC) on the market. I’ve taken some liberties with some of the assumptions since Amprius hasn’t disclosed cost and safety metrics. On safety, Amprius is not solid state and uses the same configuration of polymer separator and liquid electrolyte as current battery cells on the market (as far as I understand). In addition, they pack more energy so it stands to reason that they are going to be as safe or slightly less safe than cells that currently exist on the market. In terms of cost, again, there’s been no disclosure on this front, but it makes sense that silicon nano-anything is going to be pretty expensive…and that’s before we consider that Amprius hasn’t reached economies of scale yet.

In essence, Amprius chases energy density at the expense of everything else. And that’s okay. Differentiating and dominating a product niche is a perfectly fine way to do business and they can be very successful in that approach.

So let’s think of products that require energy density above all else - especially at the expense of cost and cycle life.

Consumer electronics immediately comes to mind as a decent fit. Amprius could charge $1,000 per kWh (10x the typical cell cost) and it wouldn’t really matter when they’re selling 5 Ah batteries (roughly $20 per device). And if it comes with the benefit of doubling your cell phone battery life, it might be worth having your battery replaced every couple of years. Phones might be the worst fit of the CE space because of their heavy usage, but things like electric power tools might be a great fit.

Drones have also been a hot topic this past year. This was Amprius’ initial target market, partnering with Airbus’ high altitude drone division. And lately, military applications have been getting a lot of buzz. In both application, energy density is paramount above all else. Especially for attritable scenarios in defense, cycle life doesn’t matter much at all. Amprius is a very good fit here.

The EV market is a tough sell. Obviously, their power and energy solutions are DOA since cycle lives fall well short of the EV target of 800 cycles. Their balanced cell hits that threshold (more or less), but the energy density metrics aren’t strong enough to offset the likely increase in cost - unlike consumer electronics, cost basically trumps every other metric for vehicles (this is largely why LFP cells have already won over NMC - people like to complain about range…until they have to pull out their wallets).

I also often see general aviation (and eVTOLs) touted as a potential fit. I don’t think Amprius offers a good fit here at all. I’ve run a unit economics exercise for an eVTOL operation, and the metric to look at for battery consideration is cost per cycle. Being that Amprius’ cells cost more and have shorter lives, that metric ends up being an order of magnitude higher than typical legacy cells, which could effectively double ticket prices for a domestic eVTOL operation. Amprius may be a good fit for auxiliary power applications, but likely not for primary propulsion applications - at least, not for high cadence operations or anywhere unit costs matter.

Of course, there are other markets as well - robotics, LEVs (i.e., e-bikes), etc. - that might also be a decent fit. This list above isn’t meant to be exhaustive.

Valuation

Today, Amprius is priced at around $1.4 billion. I won’t really look at a true valuation because I don’t feel that I know enough about their addressable markets and production costs, but we can look at the business at a high level.

In terms of scale and maturity, Amprius is currently the leader of the pack in manufacturing footprint. They have contract engineering partnerships in place to expand their SiCore production up towards 2 GWh in available capacity. They also supply hundreds of customers, which shows good diversity, and promising that there’s that much product demand.

Doing a back of the envelope calculation, if we consider a scenario where Amprius were to charge $250 per kWh (about double what a current 21700 EV cell costs) - this is very reasonable for small scale, non-EV style devices - revenues could reach nearly half a billion dollars at full contracted capacity. Assuming an optimistic net margin of 15%, that could represent just shy of $70 million in annual profit, giving an implied price-to-earnings ratio of 20x, which would be very attractive.

Of course, they’re operating no where near those levels currently - current revenue is pacing around $80 million per year, or under 20% of the scenario posited above. In addition, their gross margins are running at 13%, so that puts a 15% net margin out of reach…for the time being, at least.

My Assessment

Amprius’ pace of scale, their product offering, and the valuation numbers actually look pretty attractive. I’m actually a little impressed to see their quarterly revenue surpass $20 million. I’d like to see more visibility on their current production rates, and their vision for scale.

Their product deficiencies continue to scare me off, however. With so much effort going into next-gen battery research (by Quantumscape, Factorial, et. al.), Amprius may be setting themselves up to get leap-frogged at some point. Any one of these companies coming out with a competing product would erode Amprius’ value proposition in the marketplace. Of course, we could have said the same thing every year for the past 5 years, and still, Amprius remains the only company selling next-gen cells to actual customers.

And one thing is certain - Amprius will probably maintain the energy density high water mark for quite some time. No other company has line of sight on numbers anywhere close to Amprius.

So I’d like to see production ramp continue to accelerate as well as further product improvement (especially in areas where they’re currently deficient).

In terms of product improvement, it seems like Amprius may be resting on their laurels. Their R&D budget is something like $10 million per year. This pales in comparison to a company like Quantumscape who continues to throw hundreds of millions at R&D every year. Amprius also doesn’t have the liquidity fire power that some of these other companies have, maintaining <$100 million in available liquidity. So it seems reasonable to expect that SiCore has reached a performance plateau, and we shouldn’t expect any meaningful leap in cycle life (etc.), for the time being.

All in all, I think Amprius is a fine company that will be confined to their corner of the market, and will be highly susceptible to competition coming on line. If competitors continue to struggle, Amprius will obviously continue to do well. If a Quantumscape does succeed in commercialization, Amprius’ market share will probably erode to end products where the marginal increase to energy density is exceedingly valuable.

In terms of competition for Quantumscape, I don’t even consider Amprius to be in the same market. I think QS can kill Amprius, but not the other way around…at least not unless Amprius can improve their product as described above.

Off Topic Note on AI

This is just a quick note about using AI for research. I’ve had mixed results in the past, and have found that hallucinations make LLMs a “decent starting point” at best and completely worthless at worst.

During this exercise, I queried Claude AI to help make the spider chart in Figure 6, and it fell into the same trap I cautioned investors about - mixing and matching specs across products and making Amprius cells appear to be much more robust than they actually are. See below for prompt and output.

This is just a reminder that these tools are fabulous for certain applications (namely coding and other structured assignments), but can fall well short for unstructured research.